Chokepoint Economics

Sources: MarineTraffic.com; U.S. Energy Information Administration

Introduction

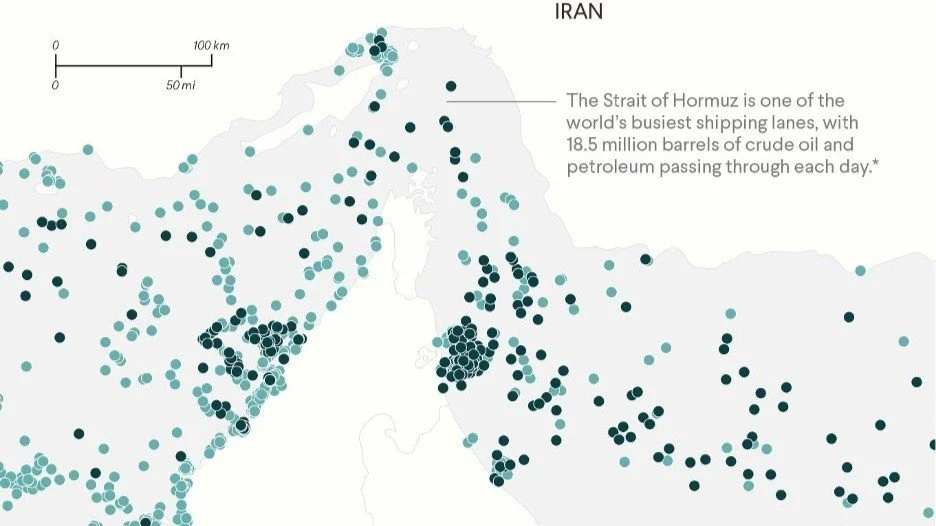

The Strait of Hormuz occupies a singular position within the architecture of the global economy. Narrow in geography yet expansive in consequence, it functions as a critical artery through which a substantial proportion of the world’s energy supply is transported. Estimates consistently indicate that roughly one-fifth of globally traded crude oil and a significant share of liquefied natural gas (LNG) pass through this corridor, rendering it indispensable to both industrialised and emerging economies alike (International Energy Agency, 2023). In periods of geopolitical tension, therefore, the Strait transforms from a logistical passage into a strategic lever, capable of transmitting economic disruption on a global scale.

The contemporary crisis surrounding the Strait of Hormuz illustrates how localized geopolitical confrontation can generate systemic economic consequences. These consequences are not confined to the immediate region but instead propagate through interconnected markets, affecting energy prices, inflation, supply chains, and financial stability. This section argues that the economic fallout from disruption in the Strait constitutes a form of indirect economic statecraft, whereby control, or the credible threat of disruption, over strategic geography produces coercive effects that extend far beyond the battlefield. Crucially, the magnitude of these effects is shaped not only by material constraints but also by perceptions of risk and uncertainty, reflecting a convergence of realist and constructivist dynamics.

Energy Market Disruption as the Primary Transmission Mechanism

The most immediate and visible economic consequence of instability in the Strait of Hormuz is disruption to global energy markets. The concentration of oil exports from major producers such as Saudi Arabia, Iraq, the United Arab Emirates, and Kuwait through a single maritime corridor creates a structural vulnerability. When this flow is threatened, markets respond rapidly. Even partial disruption has historically led to sharp increases in oil prices, reflecting both reduced supply and anticipatory speculation (Hamilton, 2013).

In the current context, interruptions to shipping and heightened risk premiums have driven price volatility rather than a simple linear increase. This distinction is important. Volatility introduces uncertainty into economic planning, discouraging investment and complicating policy responses. Energy-importing states face rising costs, effectively experiencing what can be understood as an externally imposed economic burden. As the International Monetary Fund has noted in previous energy crises, sustained increases in oil prices act as a transfer of wealth from importing to exporting states, with significant implications for global economic balance (IMF, 2022).

Moreover, the disruption of LNG flows amplifies these effects. Unlike oil, LNG markets are less flexible due to infrastructure constraints, meaning that disruptions can have disproportionate regional impacts, particularly in Europe and Asia. The combined effect is not merely an energy shortage but a broader reconfiguration of global energy distribution.

Inflationary Pressures and Macroeconomic Instability

Energy price shocks have a well-established relationship with inflation. Rising fuel costs increase transportation expenses, which in turn elevate the price of goods and services across the economy. This cost-push inflation can be particularly destabilising when it occurs in conjunction with existing economic fragilities. In the aftermath of recent global disruptions—including the COVID-19 pandemic and supply chain crises—many economies remain sensitive to external shocks.

Central banks face a complex dilemma in such circumstances. Efforts to contain inflation through interest rate increases risk suppressing economic growth, while failure to act may allow inflationary expectations to become entrenched. The result is a potential drift toward stagflation, a condition characterised by stagnant growth and rising prices. Historical precedents, notably the oil shocks of the 1970s, demonstrate the enduring economic consequences of such scenarios (Yergin, 2011).

What distinguishes the current crisis, however, is the speed at which inflationary pressures propagate. Globalisation and financial integration ensure that price signals are transmitted almost instantaneously, compressing the timeframe within which policymakers must respond. This acceleration intensifies the economic impact of disruption in the Strait of Hormuz, transforming it into a catalyst for broader macroeconomic instability.

Supply Chain Disruption and the Fragmentation of Trade

Beyond energy markets, disruption in the Strait of Hormuz affects global supply chains. Maritime transport remains the backbone of international trade, and any interruption to key shipping routes has cascading effects. Tankers delayed or rerouted around alternative pathways increase transit times and costs, while insurance premiums rise in response to perceived risk. These factors contribute to a broader increase in the cost of trade.

Importantly, the Strait is not solely a conduit for hydrocarbons. A range of industrial commodities—including petrochemicals, aluminium, and fertilisers—also depend on this route. Disruption therefore extends into manufacturing and agriculture, amplifying its economic reach. The result is a multi-sectoral shock that challenges the resilience of global supply networks.

This dynamic underscores a critical feature of contemporary globalisation: efficiency has been prioritised over redundancy. Just-in-time supply chains, while cost-effective under stable conditions, are highly vulnerable to disruption. The crisis in the Strait of Hormuz exposes this vulnerability, prompting reconsideration of supply chain strategies and potentially accelerating trends toward diversification and regionalisation.

Regional Divergence and Uneven Economic Impact

While the economic consequences of disruption are global, their distribution is uneven. States heavily dependent on energy imports—such as Japan, India, and many European countries—are particularly vulnerable. Rising energy costs strain public finances, increase trade deficits, and place pressure on domestic industries.

Conversely, some energy-exporting states may benefit from higher prices, at least in the short term. However, this advantage is tempered by the risk of prolonged instability, which can disrupt production and deter investment. Gulf economies, despite their role as exporters, are not immune. Many rely on the Strait for both exports and imports, including food supplies, making them susceptible to broader economic disruption.

This uneven impact highlights the interconnected nature of the global economy. Gains in one region are often offset by losses in another, reinforcing the systemic character of the crisis.

Financial Market Volatility and Investor Behaviour

Financial markets respond to geopolitical uncertainty with heightened sensitivity. Disruption in the Strait of Hormuz has triggered fluctuations in equity markets, shifts toward safe-haven assets, and increased volatility in currency and bond markets. These responses reflect a reassessment of risk, as investors seek to navigate an uncertain environment.

A key concept in this context is the geopolitical risk premium. This premium represents the additional cost associated with uncertainty, and it can persist even in the absence of actual disruption. As a result, the economic impact of the crisis is not limited to physical constraints but extends into the realm of perception and expectation.

This observation aligns closely with constructivist insights. Markets are not purely rational mechanisms responding to material conditions; they are also shaped by narratives, beliefs, and interpretations. The perception of risk can, in itself, generate economic consequences, reinforcing the importance of signalling and communication in managing escalation.

Realist and Constructivist Interpretations

From a realist perspective, the Strait of Hormuz represents a strategic asset whose control confers significant power. States capable of threatening or securing this chokepoint can influence global economic outcomes, using disruption as a form of coercion. The economic consequences observed in the current crisis are thus consistent with realist expectations: material capabilities and geographic positioning translate into strategic leverage.

Constructivist analysis, by contrast, emphasises the role of perception and meaning. The economic impact of the crisis is amplified by uncertainty, as actors interpret signals and adjust their behaviour accordingly. Price volatility, investor sentiment, and policy responses are all shaped by how the situation is understood, rather than solely by objective conditions.

Taken together, these perspectives provide a more comprehensive explanation of the crisis. Material disruption and perceived risk interact to produce outcomes that neither framework can fully account for in isolation.

Long-Term Structural Implications

The long-term consequences of the Strait of Hormuz crisis are likely to extend beyond the immediate disruption. States and firms may seek to reduce their reliance on the Strait by diversifying supply routes, investing in alternative energy sources, or increasing strategic reserves. Such measures, while costly, reflect a reassessment of risk in an increasingly uncertain environment.

At a broader level, the crisis may contribute to a reconfiguration of global economic interdependence. The vulnerability of critical chokepoints highlights the limits of existing systems, prompting efforts to enhance resilience. Whether these efforts lead to greater cooperation or increased fragmentation remains an open question.

Conclusion

The economic consequences of disruption in the Strait of Hormuz illustrate the profound interconnectedness of the global economy. What begins as a regional geopolitical crisis quickly evolves into a systemic shock, affecting energy markets, inflation, supply chains, and financial stability. These effects are shaped by both material realities and perceptions of risk, reflecting the interplay of realist and constructivist dynamics.

As states navigate this complex environment, the Strait of Hormuz serves as a reminder of the enduring significance of strategic geography in an era of globalisation. Its disruption underscores the capacity of localized conflict to generate far-reaching economic consequences, reinforcing its central role in both economic and security analysis.

References:

Hamilton, J.D. (2013) Historical oil shocks. Cambridge: NBER.

International Energy Agency (2023) World Energy Outlook 2023. Paris: IEA.

International Monetary Fund (2022) World Economic Outlook. Washington, DC: IMF.

Yergin, D. (2011) The Quest: Energy, Security and the Remaking of the Modern World. New York: Penguin.

Jensen, B. and Valeriano, B. (2019) ‘The cyber security dilemma’, Journal of Politics, 81(2), pp. 1–15.

Wendt, A. (1999) Social Theory of International Politics. Cambridge: Cambridge University Press.

Mearsheimer, J. (2001) The Tragedy of Great Power Politics. New York: Norton.